Unlocking Private Debt for APAC Insurers: A Regulatory Primer

Vladimir Zdorovenin, PhD

Head of International Insurance Solutions

Insurers across Asia (excluding China) face a shortage of high-quality, long-term local-currency corporate debt. Many are turning to global US dollar-denominated debt markets and increasingly considering private debt as a way to enhance portfolio yields and diversify credit exposures. The strong capital and ample liquidity of Asia Pacific insurers support a shift toward private debt. Recent and forthcoming risk-based capital regimes, together with the recently introduced IFRS 9 and 17 reporting standards, strengthen the case for private debt by rewarding stable income generation and capital efficiency.

Despite these incentives, APAC insurers allocate only 6.4% of their portfolios to private debt, far below the 35.7% average in the US and Canada and 13.1% average in Europe.1 Much of this gap reflects the perceived regulatory complexity surrounding private debt in APAC, amplified by a wave or regulatory reforms in recent years.

Here we aim to simplify these issues and help insurers navigate the private debt universe with confidence by providing clear answers to most common questions asked by APAC insurers and highlighting additional questions they may wish to raise with their private debt managers.2

No two insurers are the same – to explore how Private Debt can support your balance sheet objectives, speak with your PineBridge representative.

At a glance

Here we provide a quick overview of the key concepts, which the full primer explains in greater depth below.

Where does private debt fit in an insurer’s investment portfolio?

Private debt spans a broad set of asset classes, including corporate direct lending, asset‑backed financing, private structured finance, infrastructure debt, and real estate debt. While many APAC insurers have historically focused on higher‑return, higher‑volatility segments of the private debt universe within their alternatives allocation, global peers routinely deploy capital across the full spectrum within their core fixed income portfolios.

Is there a price to pay for harvesting the illiquidity premium?

From a regulatory capital standpoint, the illiquidity premium is effectively cost‑free for APAC insurers. Illiquid private debt typically shows more stable valuations than debt traded in liquid markets, which is useful for insurers seeking to reduce balance sheet volatility under fair‑value financial reporting frameworks.

How do I apply look‑through to private debt funds?

Most APAC regulatory regimes require – or strongly encourage – full look‑through for fund investments and impose higher capital charges when look‑through cannot be applied. Insurers therefore benefit from working with investment managers that can provide timely, detailed, and regime‑specific reporting.

Do I need credit ratings?

Under the look‑through approach, capital charges on debt investments are driven by eligible external or internal ratings, with rating admissibility criteria that differ across jurisdictions. In most APAC regimes, unrated private debt attracts capital charges in line with those on high yield debt or in between investment grade and high yield levels. Given a sufficient spread pickup, unrated private debt can often be more capital‑efficient than rated bonds.

How does fund leverage impact capital requirements?

Under the look-through approach, capital requirements for fund investments are based on changes in net asset value under prescribed regulatory stress scenarios. Higher leverage amplifies these stresses and therefore increases capital requirements on a look‑through basis.

Is there special treatment for specific types of private debt?

Several APAC regimes differentiate between “generic” corporate bonds and loans and specific forms of private debt – such as infrastructure debt, real estate debt, or private structured credit – each with its own eligibility criteria and capital treatment. Navigating these distinctions often requires support from investment managers that combine global origination capabilities with local regulatory expertise.

We plan to examine eligibility requirements and capital treatment of individual asset classes across key risk-based capital regimes in more detail in forthcoming publications.

Where does private debt fit in an insurer’s investment portfolio?

Questions for your private debt manager

Which private debt strategies do you offer?

How would you go about building a private debt solution for my balance sheet?

Private debt opportunity set

Over the past decade, private debt has expanded into a market too large for insurers to overlook. With approximately $3.5 trillion in AUM,3 the global private debt market now exceeds both the global high yield bond market ($2.8 trillion)4 and the global leveraged loan market ($1.8 trillion).5 Annual deployment into private debt is estimated at about $0.6 trillion,3 with significant flows from insurers deploying capital across the full spectrum of strategies, including corporate direct lending, asset-backed financing, private structured finance, infrastructure debt, and real estate debt.

Alternative or core?

Global insurers routinely invest across the full range of illiquid and private fixed income. While many APAC insurers still treat private debt primarily as a part of their return-seeking alternatives allocation, insurers in the US and Europe have long recognized the benefits of “going private” in their core fixed income portfolios. In the US, private placements represent 22% of life insurers’ total bond holdings.6 In the European Economic Area (EEA), illiquid and non-listed/tradeable credit accounts for 13% of insurers’ corporate bond holdings and reaches as high as 43% on average for German insurers.7

Is there a price to pay for harvesting the illiquidity premium?

Questions for your private debt manager

What is the spread pickup on your fund/strategy versus public market comparables?

How consistent has this spread pickup been over time?

Questions for your private debt manager

Do you provide look-through reporting for your fund/strategy?

Can you customize your reporting to help me meet my regulatory requirements?

Full look-through

Most APAC risk-based capital regimes encourage (and sometimes require) full look‑through to all assets and liabilities in a fund portfolio. Under this approach, insurers calculate capital charges based on the fair values, credit grades, and spread sensitivities of each underlying asset and, where relevant, liability held within funds or other investment vehicles.

Partial look‑through

Some regimes – such as Singapore, Hong Kong, and Japan’s forthcoming economic value-based solvency regulation (ESR) – allow partial look‑through for fund investments when full transparency is not available. Under partial look‑through, capital charges are based on a fund’s overall asset allocation (either the actual allocation or the worst‑case allocation allowed by the fund’s investment guidelines) rather than on individual positions within the fund. Partial look‑through almost always results in higher capital requirements than full look‑through.

No look‑through

If look‑through is not possible, an investment is typically classified as “other (non‑listed) equity.” This attracts punitive equity‑risk charges – often around 50% – which are significantly higher than the capital charges typically applied to private debt under full or partial look‑through (see Table 1 below).

To avoid unnecessary capital penalties, insurers should work with managers that can deliver timely, detailed, and regime‑specific position‑level reporting.

Do I need credit ratings?

Questions for your private debt manager

Are loans in your private debt portfolio externally rated?

Are these ratings issued by agencies that are recognized in my jurisdiction?

Are these ratings public or private?

External rating eligibility

Under the look‑through approach, capital charges for private debt portfolios and fund holdings are based on the credit quality grades assigned to individual positions. These grades are typically derived from ratings issued by external rating agencies (see Table 1 for the rating category mapping adopted under the International Association of Insurance Supervisors (IAIS) Insurance Capital Standard (ICS) for Internationally Active Insurance Groups (IAIGs)).

Table 1: Rating Category Mapping Under the IAIS ICS Risk-Based Capital Regime for Internationally Active Insurance Groups

Source: International Association of Insurance Supervisors Insurance Capital Standard Level 1 and Level 2 texts (as of 5 December 2024). Modifiers such as + or – do not affect the ICS Rating Category.

Each regulatory regime specifies which agencies may be used for credit‑grade mapping. While ratings from the three major global agencies (S&P, Moody’s, and Fitch) are universally accepted, many APAC regimes also recognize ratings from domestic agencies (e.g., JCR and R&I in Japan)8 and, in some cases, from smaller global agencies (e.g., Kroll in Taiwan and DBRS in Japan).9

Across key APAC regimes, rules governing eligible external ratings are generally more restrictive than those in the EEA, where insurers can rely on more than 20 recognized agencies,10 or in the US, where ratings from 11 SEC-registered nationally recognized statistical rating organizations (NRSROs) may be used. Insurers should therefore align private debt SMA guidelines and fund allocations with the rating agency lists recognized in their home jurisdictions.

Public vs. private external ratings

A large share of the global private debt market is rated through private letters – confidential credit assessments provided only to designated investors. Most APAC risk‑based capital regimes do not differentiate between public and private external ratings. However, a few jurisdictions impose restrictions. Australian insurers must obtain supervisory approval before using private ratings;11 under the forthcoming Japan ESR, only publicly available credit ratings will be eligible.12

Internal ratings

Insurers in Australia, Hong Kong, and Singapore may use internal credit ratings for risk‑based capital purposes, subject to regulatory approval of their internal rating models. Internal ratings can reduce implementation costs for private debt strategies and ensure that assessments reflect an insurer’s sector- or region-specific underwriting expertise.

The benefits of internal ratings must be weighed against the initial and ongoing costs of developing, validating, and maintaining an approved internal-rating framework. A pragmatic solution could be to collaborate with an external manager to leverage their existing credit grading methodologies.

What about non-rated debt?

Many private debt borrowers do not carry public ratings. Obtaining private ratings for every loan in a diversified portfolio can be expensive, and building out comprehensive internal rating capabilities may be even more resource‑intensive.

However, regulatory capital treatment for non‑rated private debt is manageable across key APAC markets:

Australia: Non‑rated corporate debt investments attract the same asset‑risk charge as BB rated corporates.

Hong Kong and Singapore: Spread risk charges for non-rated corporates are lower than those on comparable sub-investment-grade debt.13

Japan and Taiwan (forthcoming 2026 regimes), Malaysia (forthcoming 2027 regime): Corporate debt investments will carry market risk charges for non-default spread risk (calculated as a function of the current spread level on the instrument but independent of the instrument rating) and credit risk charges (based on credit grade and effective maturity). Based on draft rules, credit risk charges for non-rated corporate debt are positioned between those for BB rated and B rated corporate borrowers. For most deals, the additional capital requirements will be more than offset by spread premium relative to investment grade bonds.

South Korea: Credit risk charges for non-rated corporate debt investments are in between BB rated and B rated corporates.

Thailand: Non-rated corporate debt is treated as equivalent to that rated B or lower, resulting in relatively high capital requirements.

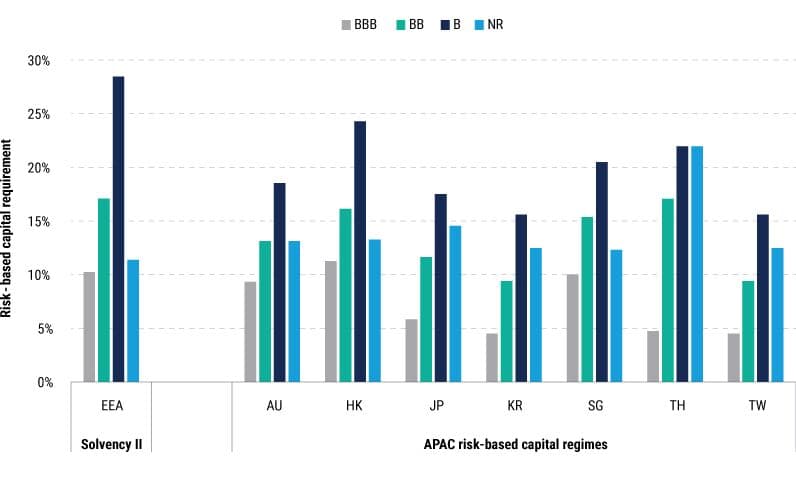

Figure 1: Risk-Based Capital Requirements for a 5-Year Corporate Debt Investment by Rating

Source: PineBridge Investments analysis based on PineBridge Investments interpretation of European Commission Delegated Regulation (EU) 2015/35 of 10 October 2014 (as of 14 November 2024), Australian Prudential Regulation Authority Prudential Standard GPS 114 Capital Adequacy: Asset Risk Charge (as of 1 July 2022), Hong Kong Insurance Authority Insurance (Valuation and Capital) Rules (Cap. 41 sub. leg. R) (as of 1 July 2024), Japan Financial Services Agency経済価値ベースのソルベンシー規制等に関する保険業法施行規則の一部改正(案) (as of 23 July 2025), South Korea Financial Supervisory Service Insurance Business Supervision Implementation Rules Appendix 22 - 지급여력금액 및 지급여력기준금액 산출기준(제5-7조의3 관련) (as of 31 March 2025), Monetary Authority of Singapore Notice 133 Valuation and Capital Framework for Insurers (as of 14 June 2024), International Association of Insurance Supervisors Insurance Capital Standard Level 1 and Level 2 texts (as of 5 December 2024), Thailand Office of the Insurance Commission แบบรายงานการดำรงเงินกองทุนประจำปี-รายไตรมาส (as of 9 September 2024).

Risk-based capital requirement for EEA, Australia, Hong Kong, Singapore, Thailand, and Taiwan comprises spread risk charge. Risk-based capital requirement for Japan and South Korea comprises credit risk charge and non-default spread risk charge, adjusted for diversification between the two.

How does fund leverage impact capital requirements?

Questions for your private debt manager

Does your fund/strategy use leverage?

What are the average and maximum permitted levels of leverage for your fund/strategy?

Under all risk‑based capital regimes, look-through capital requirements for a fund investment increase in line with fund’s leverage.

Capital charges are calculated based on the estimated change in net asset value under prescribed market stress scenarios. For a levered fund, spread risk capital scales proportionally with leverage: a fund that borrows one dollar for every dollar of equity will generally attract roughly twice the capital charge of an unlevered fund holding the same assets.

Insurers seeking to maximize regulatory capital efficiency may find it more efficient to create low‑cost leverage on their own balance sheets – such as by borrowing against high‑quality liquid assets intended to be held to maturity – and deploy the proceeds into unlevered private debt funds. At the same time, fund‑level leverage can still be a useful tool for targeting higher returns without introducing the operational complexity and additional risks of on‑balance‑sheet leverage.

Is there special treatment for specific types of private debt?

Infrastructure debt

Questions for your private debt manager

Do you offer infrastructure debt capabilities as a standalone strategy and/or as a building block for tailored multi-sector solutions?

Can you help me assess your infrastructure debt investments against my local regulations?

Under most APAC risk‑based capital regimes, qualifying non‑rated infrastructure debt typically attracts lower capital charges than comparable non-rated corporate bonds. Several regimes also introduce lower capital charges for qualifying investment-grade-rated infrastructure debt. However, the definition of “qualifying infrastructure” varies across regimes, requiring detailed assessment of each investment against local regulatory criteria.

In general, qualifying infrastructure debt finances the construction or operation of physical assets that provide or support essential public services and generate stable, predictable cash flows. Some regimes impose additional conditions, such as closed-ended lists of qualifying industry sectors or geographic restrictions on the location of infrastructure assets (e.g., domestic‑only, developed markets, OECD countries, or global). In Singapore, regulators are also trialing a distinct capital treatment for eligible debt investments in sustainable infrastructure.14

To benefit from preferential capital treatment, insurers – or their investment managers – must evaluate each infrastructure debt opportunity against the relevant qualitative criteria in the applicable regime. Investments that do not meet these criteria are typically treated as corporate debt exposures (or as securitized credit when structured as such).

Table 2 summarizes the regulatory treatment of infrastructure debt across key markets.

Table 2: Regulatory Capital Treatment of Infrastructure Debt Investments Across Key Global Jurisdictions

Source: PineBridge Investments analysis and interpretation of national legislation and insurance regulations as of 31 December 2025. IAIG – internationally active insurance group; EEA – European Economic Area. *Under Thailand RBC 2, loans for infrastructure projects carry higher credit risk capital charges than same-rating debt securities investments.

Real estate debt

Questions for your private debt manager

What are the loan underwriting criteria of your real estate debt strategy?

What are the mechanisms and structures in place for seizing collateral in the event of default?

The regulatory capital treatment of mortgage loans varies meaningfully by regime. In some jurisdictions, mortgages form a distinct asset class with their own capital requirements, and high‑quality mortgages often attract lower capital charges than comparable investment grade or non‑rated corporate debt. In others, mortgage collateral may be recognized as a risk mitigant that reduces market risk capital requirements, subject to meeting regime‑specific conditions.

Risk‑based capital regimes in South Korea and Thailand (in force) and in Japan and Taiwan (forthcoming) treat qualifying mortgage loans as a separate asset category. In these regimes, capital charges for mortgages depend on loan‑level loan-to-value (LTV) and debt service coverage ratio (DSCR) metrics. High‑quality commercial and residential mortgages can receive lower capital charges than investment grade corporate debt.

In most other jurisdictions, mortgage loans are classified as corporate loans secured by collateral. In limited cases, sufficiently strong collateral can reduce capital requirements, but this typically requires:

clear ability for the insurer to seize collateral in a default scenario, and

evidence that collateral value is not closely correlated with borrower creditworthiness.

These conditions are difficult to satisfy for pooled investment vehicles, meaning that conventional mortgage funds are unlikely to qualify for reduced capital treatment. Separately managed accounts or fund‑of‑one structures may allow case‑by‑case assessment.

Structured credit

Questions for your private debt manager

Do you offer private debt investments via structured vehicles?

Do these structures engage in pooling and tranching of credit risk?

Are debt tranches issued by structured credit vehicles externally rated?

The rapid expansion of the private debt market has led to a wide range of structured investment vehicles designed to help investors fine‑tune their risk exposure, including rated fund feeder vehicles and private securitizations. For insurers operating under look‑through regulatory capital regimes, these structures often do not provide capital relief. However, they may still help meet other insurance‑specific objectives, such as matching-adjustment eligibility, reinsurance collateral requirements, or minimum investable rating thresholds.

Rated fund feeders

In a typical rated fund feeder structure, an investor purchases rated debt notes issued by the feeder vehicle and simultaneously invests pro rata in the feeder’s equity. The feeder then deploys capital into a master fund or co‑lends alongside a private debt platform. Because investors hold both the debt and equity – a “vertical slice” of the feeder vehicle’s liabilities and capital – they also retain full economic exposure to the vehicle assets, i.e., the underlying loan portfolio. Economically, there is no tranching of credit risk between investors.

For regulatory capital purposes, in the absence of credit risk tranching, insurers can generally disregard the feeder structure and look through to the underlying loan exposures. For a typical portfolio of relatively short-dated private debt loans, capital requirements calculated on a look‑through basis are lower than the weighted average of those derived for the rated feeder‑vehicle debt (which often has a long final contractual maturity aligned with the final contractual maturity of the master fund) and equity (usually treated as capital‑intensive “other equity”).

Private debt securitizations

A private debt securitization pools privately originated loans into a securitization vehicle that issues multiple tranches of debt and a residual equity tranche – similar in form to a traditional broadly syndicated loan CLO, but often with thicker mezzanine and equity layers reflecting the concentrated and illiquid nature of the debt collateral. Investors purchase individual tranches and are not required to hold a vertical slice of capital.

This results in genuine tranching of credit risk. For regulatory capital purposes, debt issued by such vehicles is typically classified as structured credit rather than corporate debt. Investment grade securitization tranches usually attract capital charges that are the same as, or higher than, those for corporate debt of the same external rating; in many jurisdictions, non‑rated and sub‑investment‑grade tranches face punitive capital charges. Some regulators set further requirements for external ratings of securitization tranches.

As a result, capital efficiency of structured private debt investments varies significantly and depends on both the specific structure and the treatment under the insurer’s local regulatory regime. Structuring private debt securitizations in partnership with a specialist insurance manager can help avoid some of the pitfalls and unlock the benefits of private debt securitizations.

Footnotes

1 Moody’s Ratings (4 June 2024) Insurers' Private Debt holdings will grow, with benefits outweighing risks

2 For a broader discussion of private debt investments for insurers, see PineBridge Investments (22 August 2024) Why Asian Insurers Are Exploring Private Debt and CLOs

3 Alternative Investment Management Association (15 December 2025) Financing the Economy 2025. Data as of year-end 2024. AIMA definition of “Private Debt” includes corporate lending as well as asset-backed lending, infrastructure debt, and real estate debt, among others.

4 Market capitalization of Bloomberg Global High Yield Index as of 31 December 2025

5 Market capitalization of Bloomberg Global Leveraged Loan Index as of 31 December 2025

6 S&P Global Market Intelligence (30 July 2025) 2025 US Insurance Investments Market Report: The power of the private markets. The 21.6% number is based on bonds with CUSIPs containing special characters that signify private placement status. Under the US National Association of Insurance Commissioners’ definition of “private bonds,” which includes freely tradable securities issued under Rule 144A, yields a “private bond” allocation of 45.6% of total bonds.

7 PineBridge Investments interpretation and analysis of Box T1.1 in European Insurance and Occupational Pensions Authority (15 December 2025) Financial Stability Report December 2025

8 PineBridge Investments interpretation of Article 3 of Japan Financial Services Agency (23 July 2025) Financial Services Agency Notice No. 77: 保険金の支払能力に相当する額及び通常の予想を超えるリスクに相当する額の算出方法に関する件

9 PineBridge Investments interpretation of Taiwan Financial Supervisory Commission (16 February 2023) 訂定「保險業辦理國外投資管理辦法第二條第一項第三款」之解釋令

10 PineBridge Investments interpretation of European Commission Implementing Regulation (EU) 2016/1800 of 11 October 2016 (with amendments as of 22 July 2024)

11 PineBridge Investments interpretation of Attachment C to Australian Prudential Regulation Authority (1 July 2022) Prudential Standard GPS 001: Definitions

12 PineBridge Investments interpretation of Article 4 of Japan Financial Services Agency (23 July 2025) Cabinet Office Ordinance No. 74: 経済価値ベースのソルベンシー規制等に関する保険業法施行規則の一部改正(案)

13 More specifically, under Singapore and Hong Kong risk-based capital regimes, spread risk capital requirement for a corporate debt investment (bond or loan) is calculated as the change in the fair value of the instrument given a prescribed stress to the credit spread on this instrument. The magnitude of the stress is determined by the credit quality of the instrument and its remaining term to maturity. For unrated debt, the stress is set as the average of stresses for BBB and BB rated debt in the same maturity bucket.

14 Monetary Authority of Singapore (13 January 2026) Pilot for Insurers Investments in Sustainable Infrastructure (“Project Verdi”)

Disclosure

MetLife Investment Management (“MIM”), which includes PineBridge Investments, is MetLife, Inc.’s institutional investment management business. MIM is a group of international companies that provides investment advice and markets asset management products and services to clients around the world. The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

All investments involve risk, including possible loss of principal; no guarantee is made that investments will be profitable. This document is solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. Views may be based on third-party data that has not been independently verified. MIM does not approve of or endorse any republication of this material. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.